Central Bank Digital Currencies

All About CBDCs

By : Bryce Paul

From : Crypto Revolution (Newsletter 191)

The world of finance is changing very rapidly, but none of it is before our eyes. It’s all under the surface. It might not matter quite yet, but soon but it will matter a lot about what kind of financial instruments you use to store your wealth, or medium of exchange you use to make purchases.

The Bank of International Settlements released this paper earlier this year (2023) to announce their plans to rebuild the world financial system using the technology and innovation pioneered in the crypto industry. Yes that’s right– they are proposing to take our beloved blockchain technology and use it against us.

The BIS is sort of like the international central bank above the regional central banks ..… the “Central Bank of central banks”. Their paper highlights key areas and goals, including tokenization of both currencies and assets, along with a unified ledger, or network of interoperable ledgers, between all banks.

CBDCs, if ever pervasive, could destroy the final shred of sovereignty, privacy, and freedom people have left with their finances.

We’ve already seen access to money and banking weaponized against political objectors with the Canadian Truckers, for example. The fear is that the new CBDC technology would make it easier for governments to turn off purchasing power globally to anyone who holds their currency, at home or abroad.

The banks are not anti-crypto. They are anti- giving up control.

Bitcoin will never be the sound money that central banks consider. They never want to relinquish the ability to print money at will to finance their objectives cheaply and easily.

But, the new blockchain-based digital money is programmable, or “smart”. Now, if they control all the validating nodes on the blockchain network, they can confiscate money at a click of a button, whether through suspension, cancellation, or erosion.

Let’s talk about the coming changes that the scary digital CBDC’s threaten…

What Is a Central Bank Digital Currency ?

Currently banks still use old technology developed in the 1960s and 1970s. These mainframes are out of date, slow, and hardly anybody alive knows how to program on or fix them. In fact, their software is coded in COBAL and BASIC, two of the earliest programming languages, and banks have reported to have a hard time finding any developers to code in these languages because they are all aging out of the workforce.

The low-level ability these central banks have right now are simple send/receive functions. However, digital currencies are “smart” and can have parameters set to take action on their own, through smart contracts.

Both a CBDC and a stablecoin are pegged to the analog currency or cash value. The difference is in the issuer. Stablecoins are issued by private companies like Circle and Tether, while CBDCs come with the guarantee from the government and central bank. In theory, this will add confidence in using the currency across a very insecure web3 environment that’s seen countless hacks for billions of dollars that are irretrievable. A CBDC would be able to restore wealth when stolen, reverse transactions, and freeze stolen funds almost instantly. Yes, depending on the platform the CBDC is built on, these may (and likely will) be usable in web3, including DeFi.

It’s not just a topic of discussion for the future. This is happening right now across the world. If you think the US won’t go this route, you’ve fallen for yet another lie. They absolutely have to, at least to keep the dollar compatible with the rest of the world financial system. To not do that is to shoot the dollar in the head themselves, which is the complete opposite of The Federal Reserve’s mission.

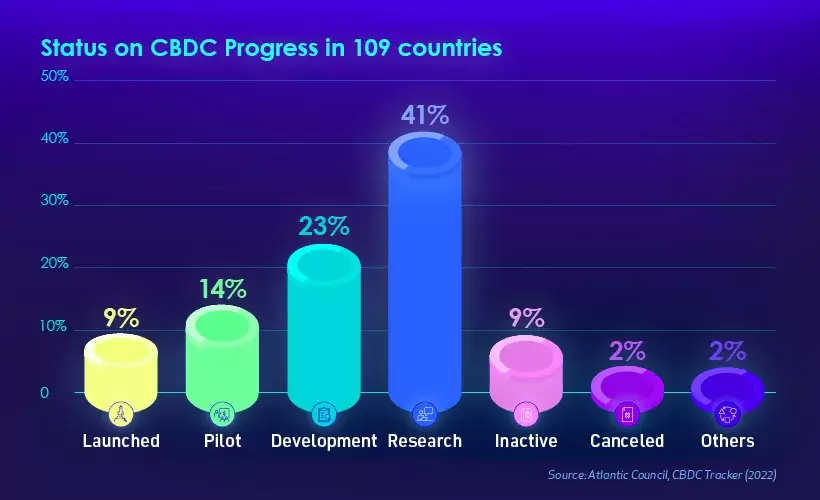

To follow progress of CBDC development, we use this tracker :

https://www.atlanticcouncil.org/cbdctracker/

65 countries have already committed efforts towards building their CBDC platform, with another 46 currently still in research. Another 16 countries finished development but are not actively using their CBDC as they were too early and the infrastructure needed isn’t ready yet.

The US will be the last to adopt this, as their system already works really well, and the political challenges of getting the public to accept this might have to wait until a digital-native generation like Gen Z is calling the shots.

One country that is ripe for change is Brazil. Brazil already has a central bank digital payments app called Pix, which has been marketed all over the country but is more popular in larger cities.

Brazil is set to roll out their Drex token on Ethereum-based Hyperledger in 2024. Only licensed custodians are permitted to create wallets. However, the central bank is encouraging hackathons and working with Ethereum Brasil to build web3 dapps that support the upcoming Drex, including DeFi exchanges. Drex supposedly offers privacy, but to whom and how remains to be seen.

What *Isn’t* a CBDC ?

There’s a lot of misinformation about the new FedNow system that just launched this year. FedNow is an upgrade to ACH (Automatic Clearinghouse) that works in the background of debit card transactions. It’s so slow and overloaded, that you see all these “Pending” status transactions on your digital bank statements. FedNow is an upgrade to that system to make final settlement throughput much faster. It is not built using blockchain technology or distributed ledger systems.

PayPal’s stablecoin PYUSD represents another major player in the stablecoin industry. Not issued by a central bank, though it shares many of the same features of authority. PYUSD is an ERC-20 token issued on the public Ethereum blockchain (as opposed to Brazil’s CBDC on Hyperledger, a private modified Ethereum).

Uniform Ledger

Currently bank ledgers are isolated by the company you deposit with. To make a wire transfer internationally, you might have to go through dozens of hops between banks to find a route that has a working relationship.

Banking relationships are like a very fractured early internet. Millions of dollars are lost/stolen every year by corrupt intermediary banks ! Yes, this happens ! There is hardly a way to trace where the funds went. Somebody just says “sorry, never got it” and runs away with it, in a sense. It’s 2023… we just can’t have that.

Retail banks are going to change form. They’re simply going to be middlemen and relationship managers, customer service desks, loan offices, and financial planners. The balance sheets will be held directly with the money issuers, the central bank of our country (or currency our country uses).

The ideal scenario for the BIS is one unified ledger that all central banks contribute to. If you’ve ever seen the General Manager of the BIS, Agustín Carstens, you’ll know why he wants everything all in one place close by.

It is unlikely that the entire world can agree upon… well, anything. The Bank of International Settlements isn’t trying to work upstream, so the most likely outcome is several different digital ledgers that are interoperable via API calls, like how most of the web works today. This is a more reasonable outcome to expect, and less globalist draconian (though not by much). The tug-o-war for web3 has some powerful new players entering the tournament, along with some names we’re already very familiar with here in the crypto space. Only time will tell if that rope will fray in two, or if one side will win full control of the world’s finances.

Supporting Technologies

Sorry to say, it doesn’t appear as if Bitcoin is part of the plan. It remains the opt-out escape hatch from all of this, rather than an integral sound money the future will be built on. At least not yet.

Ripple has been working with banks since 2018 on different pilot programs, though nothing using their systems has been announced as final. Important to note that banks using Ripplenet’s suite of products do not use the XRP token. XRP lives on XRPL, an open-source public downstream version of Ripple’s technology. Regardless, Ripple’s gone full steam ahead at trying to be the platform central banks issue their CBDCs on.

Quant (QNT) shares a similar aim but their Overledger product is designed to be an interoperability network between all financial systems. It sits as a middleware and could be that unified ledger the BIS wants. It currently supports Bitcoin, Ethereum, Ripplenet, R3 Corda, ConsenSys Quorum, Hyperledger, and they just recently added support for Polygon and Polkadot. Quant was part of a pilot between the BIS and Bank of England, in what’s known as Project Rosalind.

Quant collaborates with BIS and the Bank of England on Project Rosalind

Chainlink’s (LINK) CCIP is an interoperability layer for moving tokenized assets cross-chain. This functions more like a bridge than an issuance platform. Chainlink is by far and away the leader of connecting legacy and modern information to the world of web3. Their oracle services and price feeds are just the beginning. CCIP is an all-encompassing trusted bridge with a Risk Management Layer for moving not just money, but tokenization of anything around the world. Expect big things coming here !

We said back in 2020 that Ethereum was going to be the corporate blockchain, but that was only a stepping stone, not the final resting place. Ethereum is the global settlement chain of choice, though a CBDC would need to run on an L2 transactional layer for it to be usable.

IBM Hyperledger is an Ethereum clone, modified to suit the clients’ needs, and run on private validators. CBDCs such as Brazil’s Real are doing their pilot here. It is not known if the final version will be on the private or public blockchain. So far, it seems like institutions are more comfortable with private blockchains, for now.

Final Thoughts

Crypto technology has won, but the prize is not what we expected ..….so far ! Open source technology has been adopted, but the banks adopting this technology have discarded the original ethos.

Web3 must be a viable, usable alternative to the CBDC boogeyman that will be looming over all of us very quickly.

2030 seems to be the target for everything, so we have time to get educated, build good applications, use these applications, teach local businesses how to use decentralized financial rails, and make it through the escape hatch before it’s too late.

Money issued by central banks is only wealth for rent. Only a true digital storage of energy like Bitcoin makes sense for true wealth ownership. It could be only a matter of time before CBDC money is programmed to tell you exactly what you can and cannot buy, and from whom.

Comparison :

CBDC

Bitcoin

What money will you choose ?

Yeah, we thought so .....

The luxury of having a choice won’t last forever, though ..…

So don’t try to pick a market bottom or wait to repave your driveway.

Your life and legacy are at stake based on the decisions you make today.

All About CBDCs

By : Bryce Paul

From : Crypto Revolution (Newsletter 191)

The world of finance is changing very rapidly, but none of it is before our eyes. It’s all under the surface. It might not matter quite yet, but soon but it will matter a lot about what kind of financial instruments you use to store your wealth, or medium of exchange you use to make purchases.

The Bank of International Settlements released this paper earlier this year (2023) to announce their plans to rebuild the world financial system using the technology and innovation pioneered in the crypto industry. Yes that’s right– they are proposing to take our beloved blockchain technology and use it against us.

The BIS is sort of like the international central bank above the regional central banks ..… the “Central Bank of central banks”. Their paper highlights key areas and goals, including tokenization of both currencies and assets, along with a unified ledger, or network of interoperable ledgers, between all banks.

CBDCs, if ever pervasive, could destroy the final shred of sovereignty, privacy, and freedom people have left with their finances.

We’ve already seen access to money and banking weaponized against political objectors with the Canadian Truckers, for example. The fear is that the new CBDC technology would make it easier for governments to turn off purchasing power globally to anyone who holds their currency, at home or abroad.

The banks are not anti-crypto. They are anti- giving up control.

Bitcoin will never be the sound money that central banks consider. They never want to relinquish the ability to print money at will to finance their objectives cheaply and easily.

But, the new blockchain-based digital money is programmable, or “smart”. Now, if they control all the validating nodes on the blockchain network, they can confiscate money at a click of a button, whether through suspension, cancellation, or erosion.

Let’s talk about the coming changes that the scary digital CBDC’s threaten…

What Is a Central Bank Digital Currency ?

Currently banks still use old technology developed in the 1960s and 1970s. These mainframes are out of date, slow, and hardly anybody alive knows how to program on or fix them. In fact, their software is coded in COBAL and BASIC, two of the earliest programming languages, and banks have reported to have a hard time finding any developers to code in these languages because they are all aging out of the workforce.

The low-level ability these central banks have right now are simple send/receive functions. However, digital currencies are “smart” and can have parameters set to take action on their own, through smart contracts.

Both a CBDC and a stablecoin are pegged to the analog currency or cash value. The difference is in the issuer. Stablecoins are issued by private companies like Circle and Tether, while CBDCs come with the guarantee from the government and central bank. In theory, this will add confidence in using the currency across a very insecure web3 environment that’s seen countless hacks for billions of dollars that are irretrievable. A CBDC would be able to restore wealth when stolen, reverse transactions, and freeze stolen funds almost instantly. Yes, depending on the platform the CBDC is built on, these may (and likely will) be usable in web3, including DeFi.

It’s not just a topic of discussion for the future. This is happening right now across the world. If you think the US won’t go this route, you’ve fallen for yet another lie. They absolutely have to, at least to keep the dollar compatible with the rest of the world financial system. To not do that is to shoot the dollar in the head themselves, which is the complete opposite of The Federal Reserve’s mission.

To follow progress of CBDC development, we use this tracker :

https://www.atlanticcouncil.org/cbdctracker/

65 countries have already committed efforts towards building their CBDC platform, with another 46 currently still in research. Another 16 countries finished development but are not actively using their CBDC as they were too early and the infrastructure needed isn’t ready yet.

The US will be the last to adopt this, as their system already works really well, and the political challenges of getting the public to accept this might have to wait until a digital-native generation like Gen Z is calling the shots.

One country that is ripe for change is Brazil. Brazil already has a central bank digital payments app called Pix, which has been marketed all over the country but is more popular in larger cities.

Brazil is set to roll out their Drex token on Ethereum-based Hyperledger in 2024. Only licensed custodians are permitted to create wallets. However, the central bank is encouraging hackathons and working with Ethereum Brasil to build web3 dapps that support the upcoming Drex, including DeFi exchanges. Drex supposedly offers privacy, but to whom and how remains to be seen.

What *Isn’t* a CBDC ?

There’s a lot of misinformation about the new FedNow system that just launched this year. FedNow is an upgrade to ACH (Automatic Clearinghouse) that works in the background of debit card transactions. It’s so slow and overloaded, that you see all these “Pending” status transactions on your digital bank statements. FedNow is an upgrade to that system to make final settlement throughput much faster. It is not built using blockchain technology or distributed ledger systems.

PayPal’s stablecoin PYUSD represents another major player in the stablecoin industry. Not issued by a central bank, though it shares many of the same features of authority. PYUSD is an ERC-20 token issued on the public Ethereum blockchain (as opposed to Brazil’s CBDC on Hyperledger, a private modified Ethereum).

Uniform Ledger

Currently bank ledgers are isolated by the company you deposit with. To make a wire transfer internationally, you might have to go through dozens of hops between banks to find a route that has a working relationship.

Banking relationships are like a very fractured early internet. Millions of dollars are lost/stolen every year by corrupt intermediary banks ! Yes, this happens ! There is hardly a way to trace where the funds went. Somebody just says “sorry, never got it” and runs away with it, in a sense. It’s 2023… we just can’t have that.

Retail banks are going to change form. They’re simply going to be middlemen and relationship managers, customer service desks, loan offices, and financial planners. The balance sheets will be held directly with the money issuers, the central bank of our country (or currency our country uses).

The ideal scenario for the BIS is one unified ledger that all central banks contribute to. If you’ve ever seen the General Manager of the BIS, Agustín Carstens, you’ll know why he wants everything all in one place close by.

It is unlikely that the entire world can agree upon… well, anything. The Bank of International Settlements isn’t trying to work upstream, so the most likely outcome is several different digital ledgers that are interoperable via API calls, like how most of the web works today. This is a more reasonable outcome to expect, and less globalist draconian (though not by much). The tug-o-war for web3 has some powerful new players entering the tournament, along with some names we’re already very familiar with here in the crypto space. Only time will tell if that rope will fray in two, or if one side will win full control of the world’s finances.

Supporting Technologies

Sorry to say, it doesn’t appear as if Bitcoin is part of the plan. It remains the opt-out escape hatch from all of this, rather than an integral sound money the future will be built on. At least not yet.

Ripple has been working with banks since 2018 on different pilot programs, though nothing using their systems has been announced as final. Important to note that banks using Ripplenet’s suite of products do not use the XRP token. XRP lives on XRPL, an open-source public downstream version of Ripple’s technology. Regardless, Ripple’s gone full steam ahead at trying to be the platform central banks issue their CBDCs on.

Quant (QNT) shares a similar aim but their Overledger product is designed to be an interoperability network between all financial systems. It sits as a middleware and could be that unified ledger the BIS wants. It currently supports Bitcoin, Ethereum, Ripplenet, R3 Corda, ConsenSys Quorum, Hyperledger, and they just recently added support for Polygon and Polkadot. Quant was part of a pilot between the BIS and Bank of England, in what’s known as Project Rosalind.

Quant collaborates with BIS and the Bank of England on Project Rosalind

Chainlink’s (LINK) CCIP is an interoperability layer for moving tokenized assets cross-chain. This functions more like a bridge than an issuance platform. Chainlink is by far and away the leader of connecting legacy and modern information to the world of web3. Their oracle services and price feeds are just the beginning. CCIP is an all-encompassing trusted bridge with a Risk Management Layer for moving not just money, but tokenization of anything around the world. Expect big things coming here !

We said back in 2020 that Ethereum was going to be the corporate blockchain, but that was only a stepping stone, not the final resting place. Ethereum is the global settlement chain of choice, though a CBDC would need to run on an L2 transactional layer for it to be usable.

IBM Hyperledger is an Ethereum clone, modified to suit the clients’ needs, and run on private validators. CBDCs such as Brazil’s Real are doing their pilot here. It is not known if the final version will be on the private or public blockchain. So far, it seems like institutions are more comfortable with private blockchains, for now.

Final Thoughts

Crypto technology has won, but the prize is not what we expected ..….so far ! Open source technology has been adopted, but the banks adopting this technology have discarded the original ethos.

Web3 must be a viable, usable alternative to the CBDC boogeyman that will be looming over all of us very quickly.

2030 seems to be the target for everything, so we have time to get educated, build good applications, use these applications, teach local businesses how to use decentralized financial rails, and make it through the escape hatch before it’s too late.

Money issued by central banks is only wealth for rent. Only a true digital storage of energy like Bitcoin makes sense for true wealth ownership. It could be only a matter of time before CBDC money is programmed to tell you exactly what you can and cannot buy, and from whom.

Comparison :

CBDC

- Held by private custodians who issue wallets/addresses.

- Not private/obfuscated to governments.

- Can be frozen, canceled, or eroded (decreased if not used, eliminating savings).

- Controlled/issued at the whims of bankers.

Bitcoin

- Your keys, your crypto.

- Privacy improving/obfuscation possible.

- Bitcoin Network cannot freeze or cancel or erode your balance.

- Controlled/issued by math.

What money will you choose ?

Yeah, we thought so .....

The luxury of having a choice won’t last forever, though ..…

So don’t try to pick a market bottom or wait to repave your driveway.

Your life and legacy are at stake based on the decisions you make today.